Last week, President Trump made headlines by floating two major housing policy ideas: banning institutional investors from buying single-family homes, and directing the purchase of $200 billion in mortgage-backed securities.

Ban on institutional investors

Trump floated a ban on “large institutional investors” purchasing single-family homes.

Who exactly would this ban apply to?

We don’t know the specifics. Trump said “institutional investors,” which many people assume are groups with 1,000+ homes, but the media and policymakers discussing the issue are using different cutoffs (it could be 50 or 100+ homes), and the administration has not endorsed a specific number.

Others have used the word “corporations,” which is a very broad term that could be defined as investors who use LLCs for liability protection. Obviously, that would affect the majority of STR operators, but that broad of a definition does not seem likely. Most of the policy rhetoric is aimed at “large institutional” players, not individual investors and partnerships.

That means this proposal would likely not affect most STR investors unless they own or control hundreds of homes.

The real risk for STR investors

The real risk here is a downstream effect: additional regulation. The energy created by politicians targeting “Wall Street landlords” can easily be redirected at the local level toward “Airbnb investors” as the affordability scapegoats.

If the narrative across the country becomes “investors vs. families,” local governments may feel justified to further restrict STRs under the banner of “housing affordability”.

This framing is already a common justification used by cities to restrict or ban STRs today, and this political rhetoric could add fuel to that fire.

$200 billion purchase of mortgage-backed securities

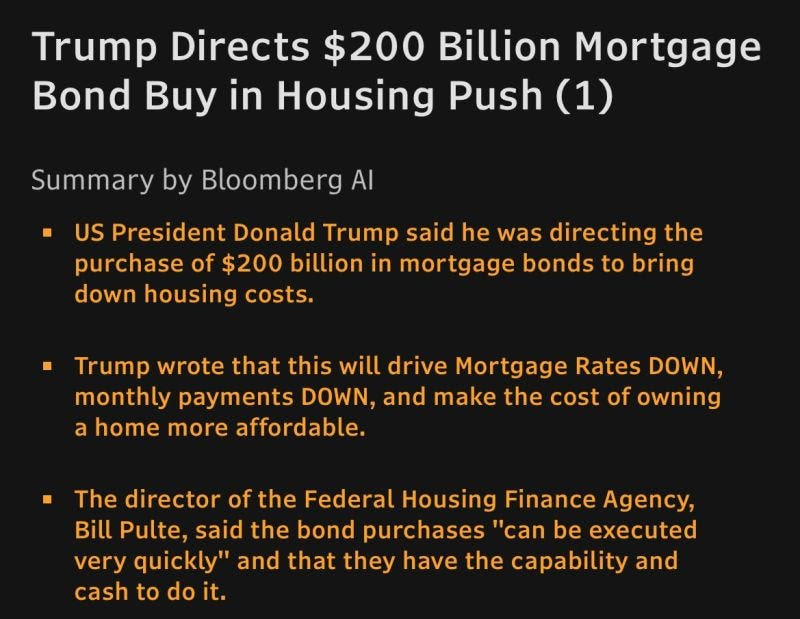

Trump also sent a social media post stating that the GSEs (Fannie Mae and Freddie Mac) would purchase $200 billion of agency mortgage-backed securities (MBS) to push mortgage rates lower and improve housing affordability.

Quick background: when large volumes of MBS are purchased, mortgage rates typically fall (all else equal). This is the same mechanism used during the 2008 housing crisis and again in 2020 during the pandemic.

Immediately after the post, mortgage rates priced in the news and had a significant drop where rates briefly fell below 6%.

In the short term, early indications suggest this could lower mortgage rates by roughly 0.25% - 1.0%. But this policy alone is not going to return mortgage rates anywhere near pandemic-era 3% levels.

The longer-term effects are far less certain. Investors may grow cautious if they believe the government is willing to repeatedly use the GSEs as a policy tool, which could introduce new risk premiums over time.

But for STR investors, if you plan to grow your portfolio in 2026, it looks like you’ll get a better mortgage rate than you would've gotten in 2025.

.webp)