Key Data's Q2 2026 performance report paints a picture of a market that’s found its floor after years of post-pandemic correction. Demand has flattened and revenue’s barely positive, but what's keeping the numbers healthy is pricing. ADR climbed 1-3% through Q1, and forward-looking rates for April through June are pacing 8-10% higher than last year.

That pricing strength is showing up in RevPAR too. Finalized Q1 RevPAR rose 2-5% year over year, and on-the-books RevPAR for the coming months is up 9-17%.

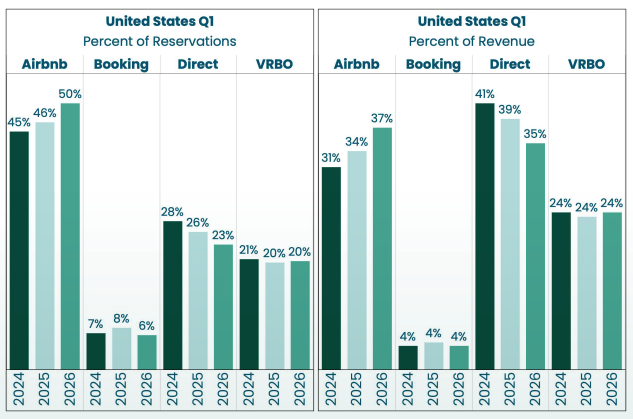

Channel Share Keeps Moving Toward Platforms

The distribution data in particular stands out. Airbnb now accounts for half of all U.S. reservations, up from 46% last year and 45% in 2024. Revenue share followed: Airbnb captures 37% of total revenue, up from 34%.

Direct bookings moved the other way. Direct fell to 23% of reservations and 35% of revenue, down from 26% and 39% a year ago. That continues a slide that Key Data flagged this time last year, and the pace has picked up. VRBO held flat at 20% of reservations and 24% of revenue.

What makes the direct booking decline stand out is that it contradicts what travelers say they want. A SiteMinder survey from late 2025 found 40% of U.S. travelers planned to book direct in 2026. But according to Key Data, the numbers say otherwise. As booking windows get shorter, travelers are choosing platforms that let them find and book quickly over seeking out individual operator websites.

Guests Are Booking Later but Staying the Same

Booking windows held mostly flat through Q1, with only minor shifts compared to last year. But the forward-looking data tells a slightly different story. April and May bookings are coming in about 4% earlier than last year, while June dipped 1%. That small expansion suggests some guests are locking in summer plans a bit sooner, though not by much.

Length of stay, meanwhile, barely moved. Q1 stays matched 2025 almost exactly, and forward data shows the same pattern holding into summer. Travelers aren't changing how long they stay, but they are changing when and where they book. This seems to be feeding into why platform share keeps growing at direct's expense.

What to Watch

The fundamentals here are encouraging. Rates are growing, forward RevPAR looks strong, and operators who have weathered the last couple years of correction are in a good position heading into summer.

The channel shift is the trend that’s most interesting. Direct is losing share year after year, and the booking behavior data helps explain why. When guests book closer to arrival, they default to wherever is fastest and easiest. For most travelers, that's Airbnb.

.webp)